From Outdated Seat Pricing to the Rule of 55: How SaaS Execs Can Future-Proof Their Business

The 2026 SaaSpocalypse ended the growth-at-all-costs era. To survive AI disruption and secure Series C funding, C-level execs must replace outdated Per Seat Pricing with value-centric models, build AI moats, target the Rule of 55 for extreme efficiency, and embrace Ecosystem-Led Growth.

The first quarter of 2026 has delivered a brutal wake-up call to the enterprise software sector. If you are a C-level executive steering a SaaS company through the MarTech, SalesTech, PartnerTech, or Data Management landscapes, the ground beneath your feet has fundamentally shifted. The recent Bank of America (BofA) Global Fund Manager Survey, alongside the violent market repricing known as the “SaaSpocalypse,” signals that the era of “growth at all costs” is officially dead.

As leaders, understanding this macroeconomic transition, recalibrating your operational efficiency, and leaning into Ecosystem-Led Growth (ELG) is no longer optional—it is the baseline requirement for securing your next funding round.

The Macro Environment: “No Landing” and Shifting Capital Flows

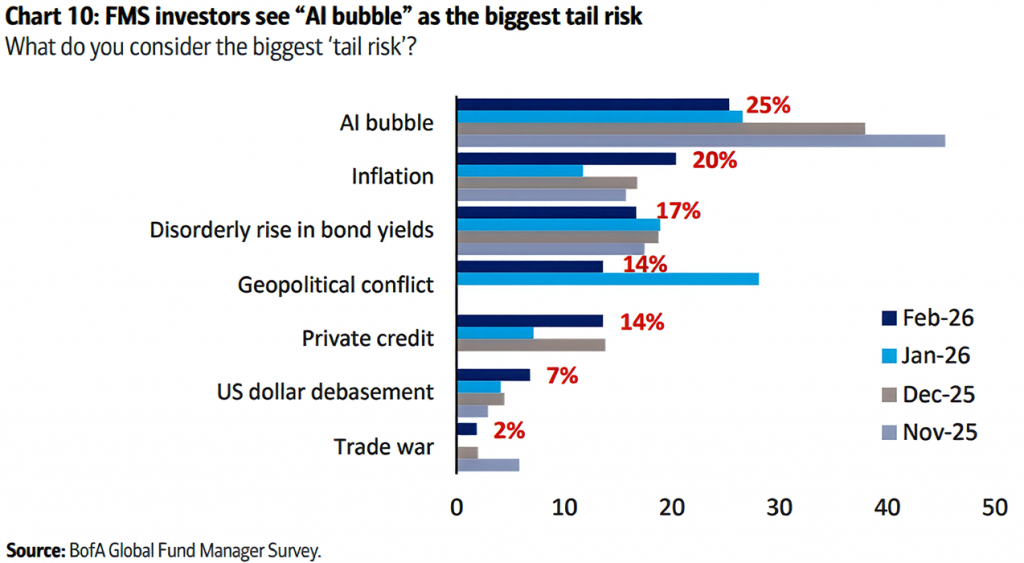

To understand what is happening to SaaS valuations, we must look at the broader capital markets. The early 2026 BofA Global Fund Manager Survey reveals an “uber-bullish” market overall, but one that is aggressively rotating capital away from traditional B2B software.

A record-high net 52% of institutional investors now base their models on a “no landing” economic scenario. In a “no landing” economy, consumer spending and growth remain robust, but inflation stays sticky, forcing central banks to maintain restrictive, higher-for-longer interest rates. For SaaS companies, this means the cost of capital remains elevated, and the discount rates applied to your future cash flows will continue to suppress high valuation multiples.

Furthermore, investors are terrified of an “AI bubble,” which 25% to 45% of surveyed fund managers cite as the market’s biggest tail risk. With hyperscalers committing an estimated $700 billion to AI infrastructure in 2026, a record 35% of investors believe companies are overinvesting in capital expenditures and demanding immediate returns. Capital is flowing toward foundational Data Management platforms and cyclical assets, leaving traditional, workflow-heavy SaaS companies in a funding desert.

Sub-Industry Risk: Where the SaaSpocalypse Hits Hardest

The SaaSpocalypse wiped out approximately $300 billion in software market capitalization in a matter of weeks. This was driven by the realization that agentic AI can bypass traditional software user interfaces, effectively ending the dominance of the “per-seat” licensing model. When an AI agent allows one employee to do the work of five, companies need fewer software licenses, leading to inevitable seat contractions.

Here is where the risk lies across your specific sub-industries:

- MarTech (High Risk to Transformation): Traditional inbound engines are failing. Standard SaaS landing pages now convert at a dismal 3.8%. If your MarTech platform relies on complex, human-operated campaign building rather than instant, AI-driven Direct Message (DM) automation and context engineering, you risk disintermediation.

- SalesTech (Medium Risk): The market is flooded with low-intent volume. Optimizing for outdated lead metrics is quietly degrading pipeline quality, making deals influenced by low-intent leads take 20% to 30% longer to close. SalesTech platforms must evolve beyond basic email sequencing toward “Emotional Forecasting”—analyzing buyer sentiment and providing real-time AI micro-coaching—to justify their value.

- PartnerTech (Advantaged but Maturing): As direct outbound channels saturate, PartnerTech is becoming mission-critical infrastructure. However, vendors must prove they can move beyond simple affiliate tracking to predictive partner churn analytics and federated data sharing via APIs.

- Data Management (Highly Advantaged): This sector is the undeniable winner. Because AI is useless without clean, governed data, investors are pouring capital into composable data mesh architectures, privacy-first governance, and cloud-native platforms.

Building Your Defensive Moat: Strategies by Sub-Industry

In an era where artificial intelligence can replicate standard software features in a matter of days, your User Interface (UI) is no longer a defensible moat. True defensibility in 2026 stems from data gravity, embedded workflows, and network effects. Here is how C-suite executives must construct structural moats against commoditization:

- MarTech: To survive, MarTech platforms must capitalize on “data gravity”—the force pulling marketing teams toward unified, cloud-based architectures rather than fragmented tool silos. Your moat is created by centralizing data on a single platform and bringing AI applications directly to where that data lives. True competitive advantage is built through “Context Engineering”—combining the reasoning of LLMs with pristine, proprietary data pipelines to execute real-world, personalized actions that generic AI simply cannot access.

- SalesTech: The legacy text-based CRM is obsolete; the new moat is a multi-modal (text, voice, video) intelligence layer. High-performing SalesTech companies are building defensibility through hybrid human-AI orchestration. By deploying AI agents that proactively handle deep prospect research and first-touch personalization, while simultaneously instituting strict governance guardrails to prevent AI hallucinations and confidential CRM data leakage, platforms cement themselves as highly trusted, indispensable infrastructure.

- PartnerTech: The ultimate defense against AI disruption is the Network Effect. PartnerTech must transition from managing linear partner programs to becoming the core “ecosystem operating system.” By facilitating shared intelligence, co-selling workflows, and joint visibility among diverse vendors and agencies, you create immense switching costs. An AI agent cannot easily replicate or replace a deeply integrated, human-and-digital partnership network.

- Data Management: This sector’s moat relies heavily on delivering “AI-ready data.” While competitors chase flashy AI pilot programs, sustainable value is found in foundational data management, strict governance, and semantic richness. Platforms that successfully combine flexible scaling frameworks—such as the Medallion Architecture (Bronze-Silver-Gold) for data refinement—with stringent, AI-enforced privacy and compliance controls will become the undisputed core of the enterprise.

The Investor Rethinking: From the Rule of 40 to the Rule of 55

To maximize returns, investors have fundamentally rewired their expectations. During the zero-interest-rate phenomenon, hypergrowth was enough. Today, buyers and venture capitalists demand sustained growth combined with extreme cash generation.

The industry standard “Rule of 40” is actively evolving into the “Rule of 55”. Because AI naturally lowers the cost of execution, basic coding, and content generation, boards of directors expect your growth rate plus your profit margin to exceed 55%. Marketing and operations value is no longer measured by sheer output, but by “strategic velocity”—the speed at which your organization can turn market signals into coordinated, revenue-generating action with a lean team.

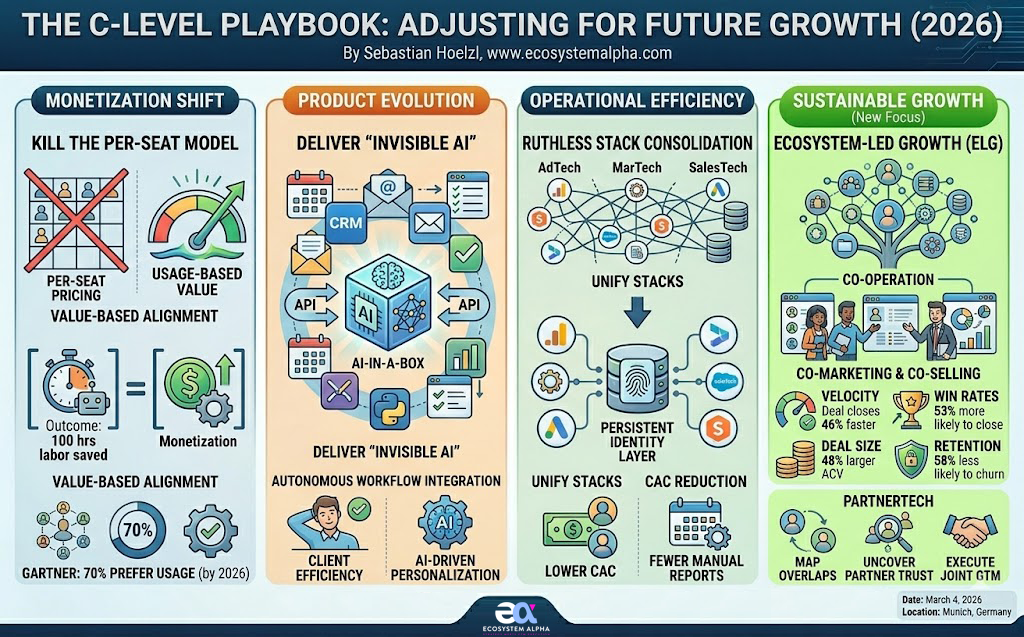

The C-Level Playbook: Adjusting the Business for the Future

To future-proof your business in this environment, C-level executives must enact immediate, structural changes:

- Kill the Per-Seat Pricing Model: You must align your monetization with the value you generate. Gartner predicts that 70% of businesses will prefer usage-based pricing over per-seat models by 2026. If your software utilizes AI to save a client 100 hours of labor, charge for the outcome or the consumption, not the human login.

- Deliver “Invisible AI”: SMBs face an “Efficiency Paradox” where they must cut costs but improve personalization without hiring. They do not want more disjointed tools; they want “AI-in-a-Box”. Your product must work autonomously in the background, embedding into their existing workflows via API.

- Ruthless Stack Consolidation: You cannot advise clients to be efficient if your own operations are bloated. Unify your AdTech, MarTech, and SalesTech stacks around a persistent identity layer to reduce manual reporting cycles and lower your Customer Acquisition Cost (CAC).

Ecosystem-Led Growth (ELG): The Antidote to B2B Friction

As traditional outbound motions fail and digital advertising costs skyrocket, the most sustainable path to efficient growth is Ecosystem-Led Growth (ELG). In 2026, no SaaS company is an island; your survival depends on how deeply integrated you are with other platforms.

ELG is the strategy of leveraging partners, integrations, and shared data to co-market and co-sell. By tapping into the established trust of your partners, you bypass the friction of cold outreach.

The data supporting ELG is undeniable for SaaS operators:

- Velocity: Deals close 46% faster using ELG playbooks.

- Win Rates: ELG opportunities are 53% more likely to close.

- Deal Size: ELG-driven deals possess a 48% larger Annual Contract Value (ACV).

- Retention: Customers sourced through the ecosystem are 58% less likely to churn because your product becomes deeply embedded in their “better together” tech stack.

Implementing ELG requires moving beyond basic referral agreements. You must utilize PartnerTech to map account overlaps securely, uncover Ecosystem-Qualified Leads (EQLs), and execute joint go-to-market motions with high precision.

De-Risking for Your Series C Investor Round

If you are preparing for a Series C round in 2026, the diligence process will be unforgiving. Investors are no longer funding theoretical Total Addressable Market (TAM) capture; they are funding market dominance and a clear, mathematical pathway to profitability. To secure funding, you must operate with near-public-company governance and flawless unit economics.

| Metric | 2026 Series C Expectation | Strategic Implication |

| LTV:CAC Ratio | Minimum 3:1 (Target 4:1) | Proves your GTM engine is highly scalable and capital-efficient. |

| Gross Margin | Target 75%+ | Demonstrates efficient service delivery despite rising cloud computing costs. |

| Net Revenue Retention (NRR) | 120%+ | Command premium valuation multiples (8x+) by proving negative churn. |

| Cash Runway | 24 to 36 months | Investors demand conservative buffers against sudden macro shocks. |

Conclusion

The 2026 software landscape is unforgiving to legacy thinking. The macroeconomic realities of elevated interest rates and AI-driven market rotations mean that SaaS businesses must adapt or die. By pivoting away from seat-based pricing, optimizing for the “Rule of 55,” and fundamentally embracing Ecosystem-Led Growth, C-level executives can build resilient, highly defensible platforms that not only survive the SaaSpocalypse but attract premium capital in the next funding cycle.

How ecosystemalpha can help your company navigate 2026

At www.ecosystemalpha.com, we specialize in helping B2B SaaS companies in the MarTech, SalesTech, PartnerTech, and Data Management sectors transition to high-performing Ecosystem-Led Growth (ELG) models. We partner directly with C-level executives to restructure outdated GTM motions, integrate your operations with high-value ecosystem partners, and optimize your unit economics to meet the stringent demands of today’s investors. Whether you are aiming to accelerate deal velocity, crush your net revenue retention targets, or de-risk your upcoming Series C funding round, ecosystemalpha provides the strategic blueprint and operational expertise to make your business definitively future-proof.