The AI Application Era: How Vertical Agents are Rewriting the Future of Work in 2026

By Sebastian Hoelzl,

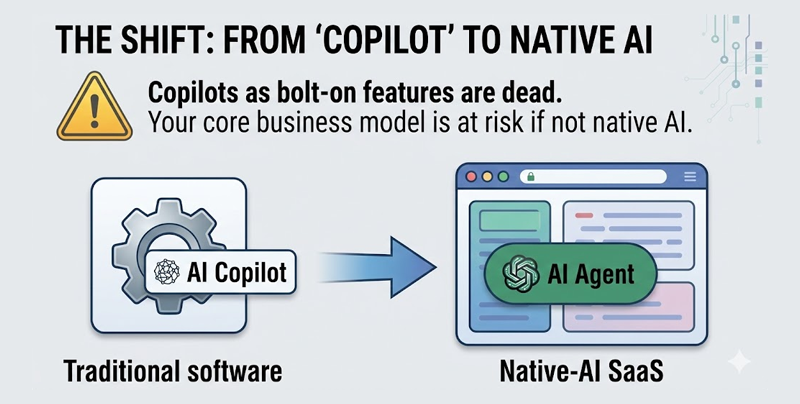

The AI “bolt-on” is dead. In 2026, hyper-specialized Agentic AI owns entire workflows. Vertical Agents are disrupting MarTech and SalesTech, forcing SaaS leaders to rethink their business models and GTM strategies now or risk total extinction.

For C-level executives navigating the Software-as-a-Service (SaaS) landscape in March 2026, the narrative around artificial intelligence has fundamentally shifted. If your strategic roadmap still treats AI as a bolt-on “copilot” feature to justify a per-seat price hike, your core business model is already at risk.

We have officially entered the era of hyper-specialized, vertical AI agents. Tech giants and foundation model builders are aggressively moving up the application stack, bypassing traditional APIs to own the enterprise workflow entirely. For leaders in MarTech, SalesTech, PartnerTech, and Data Management, this pivot presents an intensely deflationary threat to legacy software markets, while simultaneously offering an unprecedented opportunity to restructure go-to-market strategies and corporate headcounts.

The Application Cascade: Foundation Models Move Up the Stack

Between late 2025 and early 2026, a “chronological cascade” of product releases permanently altered the enterprise SaaS ecosystem. Foundation model developers stopped waiting for independent SaaS vendors to build on their infrastructure and began deploying full-fledged application layers:

- Anthropic’s Market Shockwave: In February 2026, Anthropic released open-source “Claude Cowork” plugins specifically tailored for legal workflows (NDA triage, contract review, compliance checks). This effectively commoditized the workflow wrappers that legacy legal-tech companies relied upon, instantly wiping $285 billion off the market capitalization of incumbent data and software providers. Meanwhile, their Claude Code agent now authors an estimated 4% of all public GitHub commits globally.

- Google’s “Agent-First” IDE: Google responded with Antigravity, an integrated development environment built on Gemini 3 Pro. It features a “Manager View” that allows developers to orchestrate multiple autonomous agents in parallel to plan, execute, and verify complex codebase changes.

- OpenAI’s Enterprise Alliances: Recognizing that Fortune 500 deployment requires systemic workflow redesign, OpenAI launched “Frontier Alliances.” By partnering with consulting heavyweights like McKinsey, BCG, Accenture, and Capgemini, OpenAI is embedding its agentic platform directly into enterprise systems, circumventing traditional SaaS middleware.

The SaaS Evolution: MarTech, SalesTech, PartnerTech, and Data Management

For SaaS executives, the widespread deployment of these vertical agents is forcing a fundamental architectural shift. We are moving from “AI-enabled SaaS” to “native-AI SaaS” built from the ground up around autonomous agents. This is fundamentally upending traditional per-seat SaaS pricing, driving vendors toward consumption-based token billing and outcome-oriented models.

Nowhere is this more evident than across the enterprise revenue engine:

- MarTech & SalesTech: Marketing and sales are shifting from static, scheduled campaigns to autonomous execution. By early 2026, over 90% of marketing organizations are utilizing AI agents. In SalesTech, autonomous AI Sales Development Representatives (SDRs) now handle lead research, multi-channel outreach, and dynamic sequence optimization, significantly driving down blended customer acquisition costs (CAC). Most disruptively, we are witnessing the dawn of “agent-to-agent commerce,” where consumer AI assistants negotiate directly with a brand’s retailer AI agents in milliseconds, fundamentally changing digital discovery and demanding entirely new MarTech architectures.

- PartnerTech: Traditional, linear partner portals are dead. Modern Partner Relationship Management (PRM) platforms are leveraging agentic AI to orchestrate dynamic, multi-directional partner ecosystems. AI agents are now used to automate tedious partner onboarding, securely govern co-branded asset generation, and utilize predictive insights to auto-match channel partners with the specific deals they are most likely to close.

- Data Management: Agentic workflows instantly collapse if fed poor or unstructured data, making data management the ultimate bottleneck—and most lucrative opportunity—for enterprise AI adoption. In 2026, AI-driven data ingestion tools are eliminating manual ETL (Extract, Transform, Load) pipeline engineering, allowing data to be mapped and governed autonomously. Simultaneously, autonomous data analyst agents are inspecting enterprise schemas and utilizing “natural language-to-SQL” capabilities to democratize predictive analytics across the C-suite.

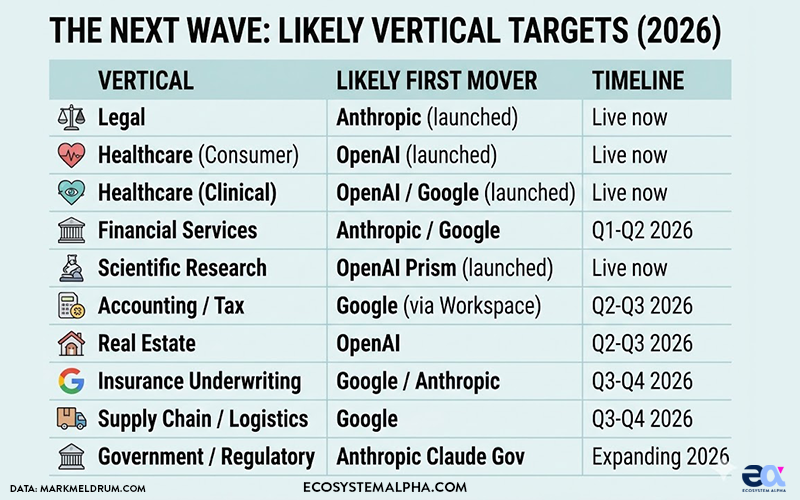

The Next Wave: Likely Vertical Targets for 2026

For SaaS founders and investors, understanding where the hyperscalers are aiming next is critical for survival and capital allocation. Based on the current trajectory and revenue incentives, we can anticipate a rapid expansion into new enterprise sectors over the next 6–12 months.

The major platforms are systematically moving down the list of high-value, data-intensive industries. The following table outlines the expected timeline and likely first movers for these upcoming vertical targets:

| Vertical | Current Status | Likely First Mover | Timeline |

| Legal | Anthropic (launched) | Anthropic | Live now |

| Healthcare (Consumer) | OpenAI (launched) | OpenAI | Live now |

| Healthcare (Clinical) | OpenAI (launched) | OpenAI / Google | Live now |

| Financial Services | All three (emerging) | Anthropic / Google | Q1-Q2 2026 |

| Scientific Research | OpenAI Prism (launched) | OpenAI | Live now |

| Accounting / Tax | Not yet targeted | Google (via Workspace) | Q2-Q3 2026 |

| Real Estate | Early exploration | OpenAI | Q2-Q3 2026 |

| Insurance Underwriting | Not yet targeted | Google / Anthropic | Q3-Q4 2026 |

| Supply Chain / Logistics | Not yet targeted | Q3-Q4 2026 | |

| Government / Regulatory | Anthropic Claude Gov | Anthropic | Expanding 2026 |

As the timeline indicates, the immediate battlegrounds are Financial Services and Accounting/Tax, followed closely by Insurance Underwriting and Supply Chain Logistics in the latter half of the year. SaaS companies operating in these spaces must rapidly build defensible data moats before the platform giants arrive.

Why the Sudden Rush to Vertical Apps? (And the Impending Pricing War)

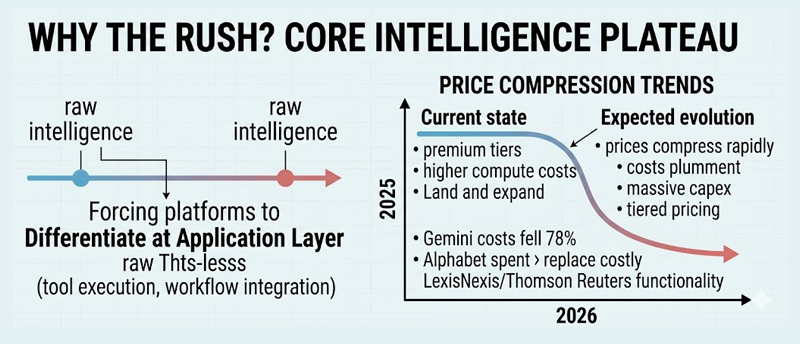

The frantic pace of vertical product releases is driven by a fundamental technological reality: core text intelligence has hit a plateau. With foundational models reaching competitive parity, tech giants can no longer rely on raw intelligence as their primary moat. They are forced to differentiate at the application layer, focusing on tool execution and deep workflow integrations.

For SaaS executives, the most critical dynamic to monitor is the evolution of AI pricing strategy. The current pricing approach reflects early-market dynamics that will soon shift violently:

Current state: Vertical AI tools are generally gated behind higher-tier subscriptions. Anthropic’s Cowork plugins require Pro or Max plans. OpenAI’s Frontier has undisclosed enterprise pricing. Gemini Enterprise is sold as a paid seat license. This premium positioning reflects both the higher compute costs of agentic workflows and a land-and-expand strategy targeting early-adopter enterprises willing to pay for competitive advantage.

Expected evolution: Prices will compress rapidly for three reasons.

- Foundation model costs are plummeting—Gemini serving costs fell 78% in 2025.

- Competitive pressure will force parity pricing as platforms match each other’s vertical offerings.

- The platforms need massive volume to justify their massive infrastructure investments (Alphabet alone is spending $175–185 billion in 2026 capex).

Expect a move toward tiered pricing: basic vertical capabilities included in standard subscriptions, with premium features (custom integrations, dedicated support, higher usage limits) at enterprise pricing.

Longer term: The vertical AI products will follow the SaaS playbook—per-seat or usage-based pricing that undercuts incumbent software by 50–80%. This is exactly what spooked the market: Anthropic’s legal plugin, offered as an open-source GitHub repository, can replace functionality that Thomson Reuters and LexisNexis charge thousands of dollars per year to provide.

The Great Re-Tasking and the Cognitive Floor

Finally, as you implement these tools internally, be aware of the “Great Re-Tasking.” Enterprise productivity is surging by an average of 11.5%, while net headcount is being reduced by 4%. The market is aggressively hiring “AI Orchestrators” and “Human-AI Collaboration Specialists” at a massive wage premium.

However, researchers are observing a widespread deterioration of critical thinking abilities among heavy AI users—a phenomenon termed “cognitive debt.” As a leader, you must establish a “Cognitive Integrity Threshold” (CIT) for your workforce. Your teams must leverage AI to accelerate their output, but they must fiercely protect and practice their own strategic, critical thinking to stay above the cognitive floor.

The winners in the 2026 SaaS economy will not necessarily be the companies with the best standalone applications, but those who successfully orchestrate AI as a collaborative, deeply integrated cognitive infrastructure.