The International GM’s Mandate: Re-Architecting GTM for EMEA Resilience and NRR

By Sebastian Hoelzl,

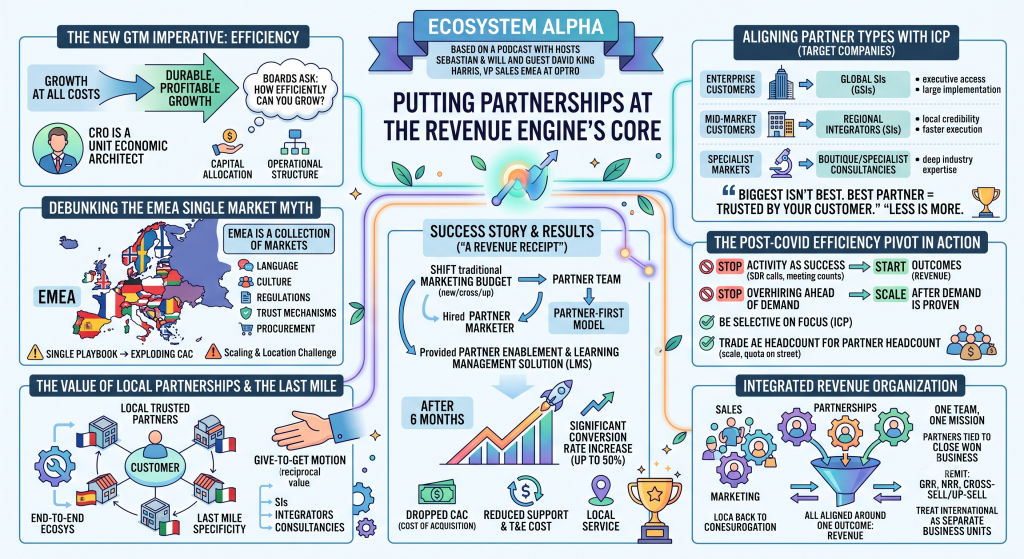

David King-Harris, VP Sales International at Optro, explains why running EMEA as one market with direct sellers inflates cost. The efficiency winners trade some headcount for local partners who carry trust, cut acquisition cost, and win retention.

The EMEA partner strategy that cuts CAC and lifts NRR

Most software companies still treat EMEA as one market and staff it with direct sellers. The leaders winning on efficiency now trade some of that headcount for local partners who carry trust, cut acquisition cost, and keep customers longer. Here is how that shift works.

The boards funding go to market in 2026 have changed the question they ask. They no longer count how many sellers you hired. They ask how efficiently you can grow and how durable that growth is. For any leader carrying a European number, that question exposes a costly assumption baked into most expansion plans: that a North American direct sales model will travel. It does not. The way you answer decides whether your cost of acquisition compounds or collapses.

EMEA is a collection of markets, not one

The first mistake is treating EMEA as a single market. It is a set of markets with different languages, cultures, rules, procurement habits, and ways of building trust. What works in Texas does not automatically work in Germany, and what works in Germany does not carry to Saudi Arabia. Companies that launch with one playbook watch acquisition cost explode in specific countries and cannot explain why. David King-Harris frames it plainly. EMEA is not only a scaling challenge, it is a location challenge, where every opportunity arrives at a different cost and often a different pace. The fix is not a bigger direct team. It is a local presence built through partners who already hold the trust a visiting seller cannot manufacture. In France, Spain, and Italy especially, local partners carry weight and can shape the market. That trust takes time to earn and cannot be shortcut with an English language playbook run from headquarters.

Match the partner to the customer, not to the logo

The strongest idea in the conversation is that the best partner is rarely the biggest one. It is the partner your customer already trusts. Reach is not the prize. King-Harris matches partner type to customer segment. Enterprise customers need global SIs for executive access and large implementations. Mid market customers need regional integrators for local credibility and faster execution. Specialist markets reward boutique consultancies with deep industry knowledge. The give to get motion holds all of it together. Referral business helps at first but dries up quickly, so partners stay active only when the value flows both ways. He learned the limit of spreading thin. Working with dozens of partners across a single region proved unmanageable and expensive. Focus on fewer, better partners beats broad coverage every time. Less is more, and it is measurable.

What the shift looks like in practice

When the mandate moved from growth at any price to efficiency, King-Harris stopped measuring activity as success. Meeting counts and top of funnel volume are inputs, not outcomes. He stopped hiring ahead of proven demand. Then he made a move he had not made before: he traded a share of AE headcount for partner headcount, keeping quota on the street while gaining scale one seller cannot provide. In one example his team moved a significant share of marketing budget to the partner team, hired a partner marketer, and went partner first in France, Spain, and parts of Central and Eastern Europe. Within six months conversion rose by up to 50 percent in some countries. Cost of acquisition dropped. Local partners handled level two and level three support, and travel costs fell because fewer people flew in and out. The receipt is the outcome, not the activity.

The infographic maps the full argument on one page. It connects the efficiency mandate to the EMEA market reality, shows how partner types line up against ideal customers, and walks through the revenue receipt from budget shift to a conversion lift of up to 50 percent, lower acquisition cost, and reduced support and travel spend. Use it as the quick reference for the whole model.

Efficiency, not headcount, is now the growth strategy, and in EMEA the partner network is how you buy it. Trade some direct cost for trusted local reach, match each partner to the customer who already believes in them, and measure the result in acquisition cost and retention rather than activity. Hear the full conversation with David King-Harris on the Ecosystem Alpha podcast.

Chapters

- Introduction and guest background

- Why EMEA is a collection of markets, not one

- Local partners and the last mile of trust

- Matching partner types to your ideal customer

- Where partnerships should sit in the organization

- The efficiency pivot after COVID

- The revenue receipt: partner first results

- Rapid fire and close

⭐️ Leave a Review: If you enjoyed this episode, please follow Ecosystem Alpha on Spotify and leave us a 5-star review! It helps us bring more incredible guests onto the show.